![Top 5 Maryland Vending Machine Drinks That Drive Sales [2025]](https://blazevending.com/wp-content/uploads/2025/12/Gemini_Generated_Image_ip2nkpip2nkpip2n-2.png)

Revenue follows consumption patterns. Maryland’s vending market reveals specific beverage preferences that separate profitable operators from those who stock based on assumption. The data is clear: five drink categories dominate Maryland vending sales, and operators who align their inventory accordingly see measurable performance differences.

Maryland vending machine drinks perform according to regional consumption behavior, climate patterns, and demographic distribution. This isn’t about preference—it’s about what moves.

Water dominates Maryland vending operations. In a state where 30% of the population actively tracks health metrics and bottled water consumption exceeds the national average by 14%, this category isn’t negotiable.

The numbers: Maryland operators report water accounting for 23-28% of total beverage revenue across mixed-location routes. Health-conscious demographics in Montgomery County and Howard County drive this higher—some operators see water hitting 35% in these zones.

“Water is the foundation category. Everything else fills around it. If your water allocation is below 20%, you’re leaving money on the machine.”

What moves: 16.9 oz bottles in major brands (Dasani, Aquafina, Poland Spring). Generic or regional water brands underperform in Maryland by 8-12% compared to recognized national brands.

Energy drinks represent Maryland’s second-largest beverage category. The state’s concentration of federal workers, tech sector employees, and shift workers creates consistent energy drink demand across urban and suburban markets.

Red Bull maintains category leadership, but Monster and Bang show stronger growth trajectories. Maryland vending operators report energy drinks generating $0.87 in revenue per machine slot compared to $0.62 for traditional sodas.

Geographic concentration: Baltimore City and suburbs see energy drink sales 22% above state averages. Prince George’s County follows at +18%.

Purchase patterns: Energy drinks show bimodal demand—morning rush (6-9 AM) and afternoon slump (2-4 PM). Operators who stock 4-5 slots in high-traffic locations report 30-40% faster turnover than single-slot allocations.

Cold coffee has moved from specialty to staple in Maryland vending machines. Starbucks Frappuccinos, Dunkin’ Cold Brew bottles, and Stōk Cold Brew dominate this category.

The data: Maryland coffee drink sales increased 34% between 2022-2024, with cold/iced formats accounting for 89% of that growth. Traditional hot coffee vending has declined 12% in the same period.

Demographic driver: Maryland’s median age of 38.8 years and high percentage of college-educated residents (40.2%) correlates directly with cold coffee consumption. This isn’t generational preference—it’s routine optimization for knowledge workers.

What operators miss: Cold coffee drinks generate higher per-unit revenue ($3.25-$3.75) compared to traditional sodas ($1.75-$2.25). The margin difference is significant—cold coffee produces 18-24% better gross profit per slot.

Gatorade and Powerade control Maryland’s sports drink category. In a state with 847 high schools, 14 Division I universities, and extensive recreational infrastructure, sports drinks maintain consistent velocity year-round.

Seasonal variance: Sports drink sales spike 45-60% during Maryland’s summer months (June-August) when temperatures average 85-90°F. Winter sales stabilize at baseline but never collapse—gym-adjacent locations maintain steady turnover.

“Sports drinks don’t depend on weather anymore. The category has evolved beyond athletes. It’s hydration for anyone doing anything.”

Color matters: Blue and red Gatorade variants outsell yellow/orange by 23% in Maryland markets. Operators who stock according to flavor preference rather than variety see 15-18% faster category turnover.

Coca-Cola and Pepsi products still move, but their dominance has eroded. Maryland vending operators report traditional sodas now accounting for just 15-18% of total beverage sales—down from 32% in 2019.

What survives: Coke Zero, Diet Coke, and Pepsi Zero Sugar maintain velocity. Full-sugar Coke and Pepsi show declining purchase rates except in specific high-traffic impulse locations (rest stops, convenience locations).

The shift isn’t about health trends—it’s about portfolio compression. Maryland consumers allocate their beverage purchases to higher-value categories (energy drinks, cold coffee) and reduce traditional soda consumption accordingly.

Don’t miss this: Cherry Coke and Mountain Dew perform above category averages in Maryland by 11-14%. Regional preferences persist within declining categories.

Maryland isn’t average. The state’s median household income of $90,203 (18% above national median) directly impacts vending beverage choices. Higher-income consumers purchase premium beverages more frequently—energy drinks, cold coffee, and branded water—while traditional sodas decline.

Geographic density matters: Maryland’s population concentration in the I-95 corridor creates different purchase behavior than dispersed rural markets. Urban/suburban Maryland operators see 23% higher premium beverage sales compared to national averages.

Does weather influence Maryland vending machine drinks? Yes, but not how operators assume. Maryland’s humid subtropical climate means summer peaks are real—but winter troughs are shallow. Year-round gym culture, indoor work environments, and consistent coffee consumption mean beverage sales maintain 78-82% of peak velocity during winter months.

How do Maryland demographics shape drink selection? Maryland’s diverse population (33% Black, 11% Hispanic, 7% Asian) creates preference variation within metro areas. Montgomery County beverage mix differs from Baltimore County by 15-20% across multiple categories. Smart operators test and adjust rather than apply uniform stocking across routes.

Step 1: Audit Current Beverage Allocation

Pull sales data for the last 90 days. Calculate actual revenue by category, not just unit velocity. If water is below 20% or energy drinks below 15%, you’re underperforming Maryland market benchmarks.

Step 2: Rebalance Inventory to Match Maryland Data

Target allocation for mixed-location Maryland routes:

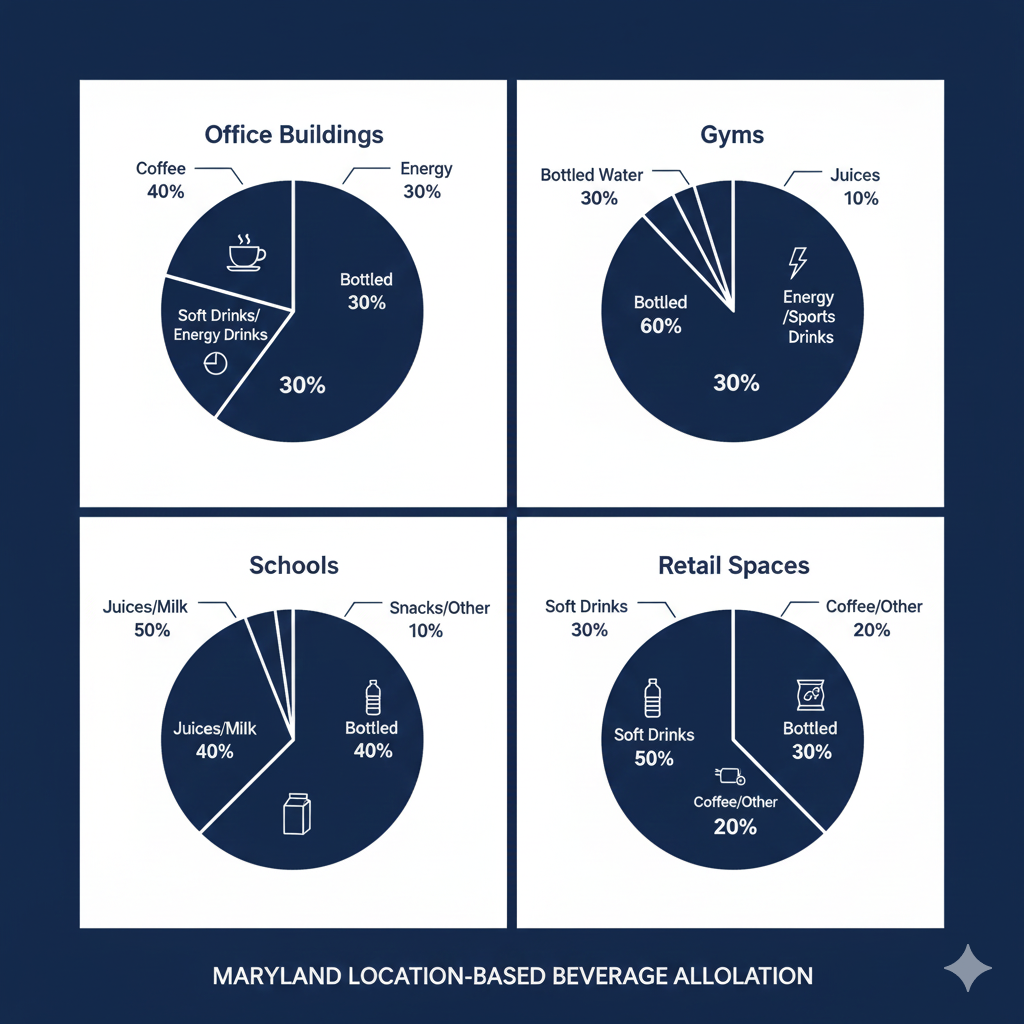

Adjust this baseline for specific location types—gyms need more sports drinks, office buildings need more cold coffee.

Step 3: Test Premium Brands First

Maryland consumers pay for recognized brands. When adding cold coffee slots, start with Starbucks and Dunkin’ products. When expanding energy drinks, prioritize Red Bull and Monster. Generic options underperform in Maryland by double-digit percentages.

Step 4: Track Seasonal Variance Without Overreaction

Monitor summer sports drink spikes but don’t reduce winter inventory by more than 20%. Maryland’s year-round fitness activity and indoor recreation sustain baseline demand even in cold months.

Step 5: Geographic Customization Within Maryland

Montgomery County and Howard County: Increase water and cold coffee allocation by 5-8 percentage points.

Baltimore City: Increase energy drink allocation by 5-7 percentage points.

Southern Maryland: Traditional sodas maintain slightly higher velocity—keep 18-20% allocation.

Snacks create baseline vending demand, but beverage selection is what amplifies revenue — temperature, hydration patterns, and impulse behavior can double conversion without changing foot traffic. That’s why I separated my full beverage analysis into its own breakdown here: Top 5 Maryland Vending Machine Drinks That Drive Sales [2025].